Shorouk Express

Chapter I

Germany’s top emitting coal power generator painted green

Norbert Winzen stares at us in surprise when we tell him that his trusted life insurance company, Allianz, is greenwashing RWE. Germany’s top polluter has made his life hard over the last years; not only has RWE poisoned the air he breathes, it has also nearly destroyed his farm in a village nestled in the wetlands of North Rhine-Westphalia.

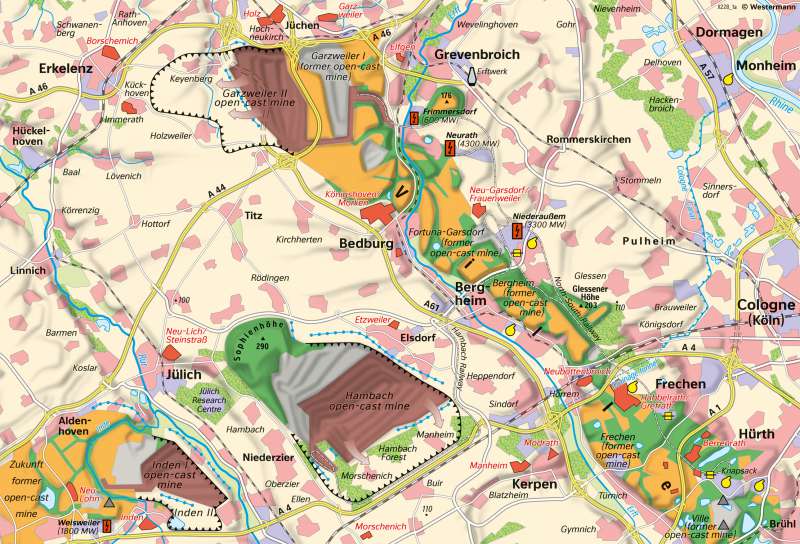

This is the fourth largest state (“Land”) in the federal republic of Germany and one of the most important industrial and energy hotspots in Europe. It took massive protests that began in 2019 to finally convince the German government to save the community of Keyenberg and Winzen’s home, halting the expansion of RWE’s Garzweiler open-cast coal mine which fuels the company’s dirtiest power plants. RWE is Europe’s second-largest coal utility and one of the continent’s biggest contributors to greenhouse gas (GHG) or carbon emissions.

Besides boosting man-made global warming, the company’s mines and coal-fired power plants pollute the air, the water and the soil. They take a heavy toll on the health of the 42 million people who live within a 200km radius, including in neighbouring Belgium and the Netherlands.

Yet RWE is featured in dozens of investment products offered by asset managers across Europe and classified as ESG, an acronym which refers to Environmental, Social and Governance objectives.

These products, commonly defined as “green” funds, are regulated by the European Sustainable Finance Disclosure Regulation (known as SFDR), which since 2021 has imposed transparency requirements aimed at diverting private capital from dirty to sustainable companies. Unfortunately, the new rules are flawed and being abused. A massive flow of investor money has gone into self-proclaimed responsible funds that are in fact propping up the planet destroyers – a.k.a. fossil fuel companies.

The EU makes way for the rush to “green” profits from coal

RWE is not the only energy producer using coal which attracts green investment, but is certainly one of the most profitable in Europe with over 28 billion euro of earnings in 2023. The EU-regulated green funds account for 3% of the company’s capital. Altogether they represent the sixth largest shareholder in terms of aggregated value. Over the past three years (2021-2024), they have earned a total of $1.6 billion by buying and selling RWE shares and pocketing the company’s annual dividends. The top 10 most profitable asset managers made over $1.3 billion (80% of the total).

This supposedly “responsible” lucrative profit was created from damage to public health which has an equally high monetary value. The comparison stems from the latest analysis by the European Environment Agency which shows that RWE’s most polluting coal-fired plants are indeed responsible for over 1.3 billion euros in health costs (almost a third of the total health costs associated with the dirtiest industrial plants in Germany across all sectors). It turns out that good returns for investors are bad news not only for the climate crisis, as we showed in our previous investigation, but also for the people affected by pollution.

Interesting article?

It was made possible by Voxeurop’s community. High-quality reporting and translation comes at a cost. To continue producing independent journalism, we need your support.

Subscribe or Donate

More than one third ($593 million) of all returns from RWE shares were secured by funds promoted with names evoking the “public good”, deliberately designed to attract investor attention. Among these profits, as much as $543 million was taken in by funds whose names include misleading terms – such as “ESG” “green”, “environment”, “climate”, “sustainable”, “impact”. The EU now wants to ban funds with these names from investing in companies that earn more than 1% of their revenue from the extraction, refining and distribution of coal. The ban was recently recommended by the European Securities and Markets Authority (ESMA).

Precisely, about 1% of RWE’s revenue comes from coal-based fuels, which carbon-intensive industries use for energy. This information was confirmed privately by RWE’s investor relations team to Voxeurop. However, most green funds currently allow investments in companies with up to 10 to 20% of revenue from coal. Because of these loose thresholds, green funds will keep investing in RWE and other coal producers until the ESMA guidelines come into effect in May 2025. Notably, the new guidelines aren’t legally binding, leaving enforcement to national regulators. A few financial institutions among those which market mislabelled funds have confirmed they’ll comply with these rules, while most of them declined to comment on their intentions.

Case study: Allianz’s dodgy fund unveils a widespread hoax

During our research into coal greenwashing, we came across the products marketed by Allianz Benelux, the Belgian subsidiary of the German group Allianz, the world’s largest insurance company and Europe’s largest financial services company. Allianz ranks second among the top 10 asset managers investing the most in RWE through EU-regulated green funds. From 2021 until the beginning of 2024, the financial giant’s exposure (through its several green funds) towards the compatriot coal champion increased by almost 47 million USD, peaking at 130 million in the last quarter of 2022.

Allianz Benelux’s offering boasts a Russian doll-like product, called Better World, which bundles together a number of separate green funds, which in turn hold shares in different companies. Checking how green such a complex portfolio is would be a headache for any unsavvy retail investor. The website’s drop-down menu links to documents with cryptic jargon copied from ESMA technical norms, with no mention of the investee companies.

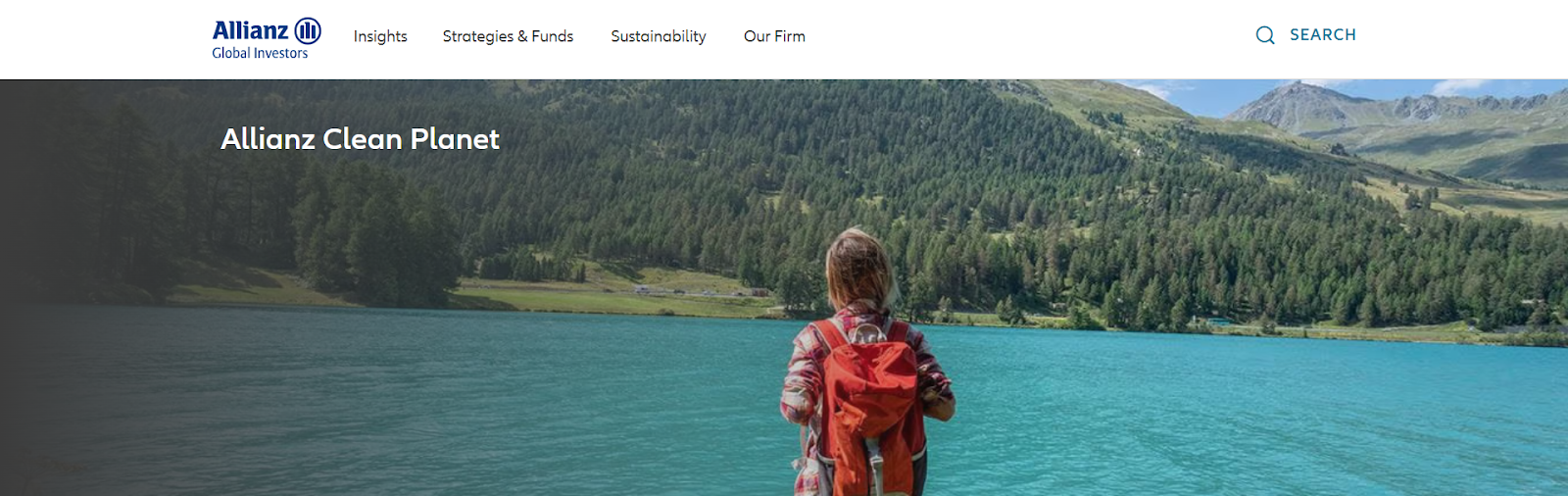

Among the funds listed in the Allianz product, one called Clean Planet happens to sponsor RWE, as we found out by analysing data extracted from Refinitiv platform (owned by the London Stock Exchange Group). This fund, which, like many others, is conveniently domiciled in Luxembourg (which imposes softer regulation and taxation) and is offered in several European countries (besides Belgium, it is available in Germany, France, Spain, Netherlands, Italy, Switzerland and the UK, among others). Its portfolio is relatively small in terms of financial value and it only started investing in RWE at the beginning of 2024 (which is coincidentally when its financial performance recovered after plummeting in 2023). As a result, the returns associated with the German utility may not yet be available, based on the latest updated data to which we had access.

According to Allianz’s website, the fund contributes to reducing air, water and soil pollution – exactly the opposite of what RWE, as an energy company, does. “The denomination ‘Clean Planet’ clearly brings to investors’ mind the promise of environmental improvement, even though the term ‘environment’ is not explicitly used in the fund name” said Axel Pierron, associate director of Morningstar/Sustainalytics, a leading investment research company. ESMA’s guidelines seem to call for a broad interpretation of fund names, so the term “clean” may well fall into the environment category.

The name of the fund and its official objective make the whole story an excellent example of green finance misinformation which involves several other financial players partaking in similar inconsistent commitments and obscure due diligence methodologies (based on their funds documentation).

“If a fund only holds 1% of its portfolio in shares of a specific company, one might argue that this is a relatively insignificant figure, however RWE is also included in the portfolios of many other investors, raising the overall investments to considerable levels,” Fabio Moliterni, a climate finance expert working at the Milan-based ethical finance company Etica Sgr, told Voxeurop. “Therefore, it is essential to examine even a single case, since it represents a phenomenon common to all funds that collectively invest billions in this company”.

How any investor can be caught in the greenwashing trap

The question we asked ourselves was: “Are investors who bought Allianz’s dodgy “green” product informed that they are subsidising RWE’s stock market and profiting from its polluting activities?”

To find the answer, which we found was “no”, we have to go back to the place where our investigation began. Welcome to Brussels, the capital of Belgium and of the European Union’s greenwashing. In September 2024 we contacted an investment adviser at Crelan, Belgium’s fifth largest bank, who also acts as a broker for Allianz products. We made an appointment by email,, in the guise of a potential client interested in the Better World product. As we stood in front of the adviser in his office, located in the middle of the European institutions, we already knew that Allianz’s Clean Planet held shares in RWE. But as it turned out, the consultant had no idea.

When we asked the Crelan consultant face to face if any of the funds included in “Better World” had any polluting or fossil fuel companies in their portfolio, the proud answer “no” came with a shake of the head. However, the broker added that he never has the full list of companies included in the funds he offers to his clients. To get this list, he would have to make a specific request to Allianz. He confirmed that other people have invested their savings in the Clean Planet fund. In our estimation, it is probable none or only a few of them know that RWE was lurking beneath the surface. Greenwashing was happening just a hundred metres from the European Commission, right under the nose of the very policymakers who put the failing SFDR legislative framework on the table.

An investment manager at the Allianz subsidiary in Belgium (who asked to remain anonymous for fear of speaking out) confirmed that investors never ask for the full list of all investee companies. “You’re the first to ask for it,” she told Voxeurop. “I don’t see the point, because it’s a matter of trust. People ask what the objectives of the fund are, but they don’t ask what’s behind it.”

A key loophole in EU legislation is that asset managers’ marketing material only need to disclose the top 15 companies in which a green fund holds the largest shares, which is exactly what the Crelan adviser did during our meeting where we posed as potential clients. Based on a separate piece of legislation, complementary to the SFDR, the full list of investee companies is publicly available in the fund’s management reports. But these reports are omitted or simply ignored by financial operators in their face-to-face interactions with investors, undermining transparency in practice.

“There is no obligation to provide the semi-annual or annual report to the investor prior to subscription,” said a spokesperson from the Belgian Financial Services and Markets Authority. “Nevertheless, the investor must be able to obtain the latest report and the prospectus free of charge, on its request, before the conclusion of the contract.”

When we posed as an investor, neither the advisor at Crelan Bank nor the investment manager at Allianz in Brussels referred to Clean Planet’s semi-annual report dated March 2024 (whose direct link is missing from the Better World website), which shows 9,263 shares in RWE being worth $313,728. The investment increased up to 12,963 shares, worth $469,057, in the second quarter of the year, according to the updated schedule we received in September 2024 from Allianz Benelux. This value represents a little bit more than 1% of Clean Planet’s portfolio. Such a relatively tiny fraction is the norm for fossil energy companies, which therefore never appear in the top 15 holdings of green funds, although they end up totalling billions across all the EU-regulated funds.

A Crelan spokesperson told Voxeurop: “Crelan does have a partnership with Allianz to promote the latter [EU-regulated funds] to its network (i.e. of clients) as a possible provider for life insurance products”. He explained Crelan received a fee from Allianz, “which is however responsible for the provision of adequate information and training to its brokers, which also include our bank agents. As for the fact that we had received limited information in our meeting, the responsibility was passed off. We were told: . “Our agent was not acting as a banking agent on behalf of Crelan, but as an independent insurance broker on behalf of Allianz, therefore we are not responsible for the fact that the agent was not sufficiently informed on the subject.”

Axel Pierron of the Morningstar/Sustainalytics rating agency acknowledged the challenge that a potential client might also face in not being fully informed. He told Voxeurop that the EU transparency rules “do not really shelter the majority of retail investors who are unable to locate and understand all the ESG-related metrics reported in fund documents from greenwashing. Financial advisors can hardly help in the process as they often lack sufficient understanding and knowledge. In fact, educating advisors on key ESG themes remains a major challenge at financial institutions.”

In October 2024 we escalated our inquiry to Allianz’s headquarters in Munich on this point; a spokesperson told us: “Our investment disclosures are fully compliant with regulatory requirements.”

Another shortcoming is that asset managers don’t have to indicate which companies are part of the investments intended to achieve the environmental or social objectives of the fund (the ESG portion).

“We do not comment on individual companies,” said the Allianz spokesperson who, nonetheless, added that the group “wants to support […] companies that commit to transition paths.” This statement implicitly suggests that RWE is included at least in the ESG portion of the Clean Planet fund (50% of the portfolio), if not also in the fully sustainable portion (90% of the portfolio) which has to follow stricter EU requirements. Indeed, the fund’s marketing material also highlights the theme of energy transition as a way to clean up the air (1). The underlying assumption is that moving away from fossil fuels and reducing carbon footprint will do good not only to the climate but also to the environment and people’s wellbeing. While this is true in principle., the reality on the ground is far more complex.

Chapter II

From smart banks to coal tanks: the human cost behind eco-marketing

Allianz customers who hope to do good through supposedly responsible investments, while earning a decent income, might be interested in finding out just how little coal mines and coal-fired power stations contribute to a “better world”. That’s why we set off on a journey 200km east of Brussels. Our destination: Cologne, the largest city in North Rhine-Westphalia and part of the most polluted urban area in Europe. Cologne and other Rhenish cities are long-standing shareholders of RWE which has historically held a tight grip on local administrations. We wanted to talk to local people affected by RWE’s activities and give them a chance to explain, from their own perspective, why Allianz’s “clean” investments in coal are not so clean.

Everyone we met was as surprised as Norbert Winzen, the farm owner in Keyenberg, to hear that RWE is such a popular bet among responsible financiers. Many of them have worked tirelessly to hold the German coal champion accountable for the harm its emissions have caused to the climate and public health. Their initiative is the RWE Tribunal, an informal civic court founded by the Cologne-based collective ATTAC. This tribunal organised four public hearings between 2021 and 2023 in which scientists, health experts and activists discussed evidence of RWE’s responsibility.

The German authorities grant RWE carte blanche

In 2022, ATTAC and other local civil society organisations supporting the RWE Tribunal handed over a petition with 4,370 signatures to a representative of the public prosecutor’s office in Cologne, in support of an indictment for manslaughter filed by more than 20 lawyers.

The criminal complaint, grounded on a ruling by the Federal Constitutional Court, was referred to the public prosecutor’s office in the neighbouring city of Essen, home to RWE’s headquarters, which rejected it in 2023. The plaintiffs appealed against the decision and in March 2024, RWE Tribunal activists gathered in front of the appeal prosecutor’s office in the city of Hamm to demand the opening of a formal investigation. However, charges were eventually dismissed a few days later.

In its decision, the prosecutor of Hamm has acknowledged that “the negative environmental effects caused by pollutants such as carbon dioxide, particulate matter, nitrogen oxides and mercury emitted during the operation of coal-fired power plants” are “undisputed and sufficiently proven” by the lawyers who sued RWE, adding however that “an administratively authorised plant constitutes neither a criminal offence nor a legally disapproved risk”.

In Cologne Dr Heinrich Comes, the lawyer who led the lawsuit, emphatically said: “No law in Germany authorises commercial activities leading to murder”. He added that “the administrative permission received by RWE cannot prevail on the rights to life and health enshrined in our constitution.” Dr Comes accused investigating bodies of “deliberately turning a blind eye, evading their legal mandate to protect citizens against a punishable crime.”

According to Dr Comes, the blame lies with members of the ERWE”s Executive Board and Supervisory Board, who “knowingly accepted that more and more people in Germany and around the world have died over the last two decades as a result of RWE’s coal mining and power generation, due both to the local impact of health-damaging toxic pollutants, and to the global impact of climate-altering carbon emissions. Modern attribution science has quantified the casualties resulting from what is happening here in the Rhenish lignite area. Although we cannot name individual victims, the statistical deaths are real deaths.”

The health impact of RWE’s plants is exacerbated by the use of lignite (or brown coal), a fuel that has a lower energy value than hard (or black) coal and therefore produces more air pollutants per megawatt when burned. Germany is Europe’s largest producer and consumer of lignite. In 2016 alone, RWE was responsible for 1,880 premature deaths in Germany and in neighbouring countries, according to a study by the Brussels-based NGO Climate Action Network. Around 65% of the deaths were attributed to the company’s largest plants in North Rhine-Westphalia (Neurath, Niederaussem, Weisweiler and Frimmersdorf), all of which are in the “Coal-Killers Europe Top 10”.

In the same year, the four plants were responsible for 1,320 hospital admissions and 30,000 days of asthma symptoms in children. These figures may well be out of date, as coal pollution has decreased over time. But in 2023, a team of German researchers found that particulate matter (PM) and nitrogen dioxide (NO2) from lignite-fired plants were still respectively responsible for the loss of between 7,800 and 13,500 years of life, roughly, among the country’s exposed population.

To put a face to those figures, we met Christian Döring, a paediatrician involved in the RWE Tribunal initiative, and his young patient Andre, a 14-year-old schoolboy from Cologne. Döring was preparing for a routine check-up with Andre, who told us that it felt like he was slightly choking when he breathed and that he coughed a lot: “The industry makes our breathing conditions worse every day. Asthmatic people like me know what I’m talking about.”

Döring explained how the pollution from lignite contributed to the overall background pollution in cities: “It exposes our citizens and increases their risk of getting sick, especially children who are born while their mothers inhaled toxic substances during pregnancy, and [who] continue to absorb them more than adults due to their faster breathing pace.”

We show Döring the Clean Planet website featuring a photo of a child breathing fresh air against a mountain backdrop. His reaction is stark. “This marketing communication is a crime against our society. We can’t invest in something that kills children. This fund should no longer be called Clean Planet. It should be called Dirty Planet,” he said, pointing to the evident hypocrisy of the image. “I cannot imagine how the CEOs of RWE and Allianz can stand in front of their own children, while putting their lives at risk.” Andre agreed with his doctor: “Adults who put their money into these funds that support highly polluting companies like RWE, which have a very bad impact on the health of their children, are basically investing in a worse future for them”.

Markus Dufner had even tougher words. He is director of the Cologne-based Association of Critical Shareholders, which submitted a motion on the ravaging consequences of lignite operations during RWE’s general assembly in 2023: “Allianz has obviously been taken in by RWE’s advertising slogan ‘Our energy for a sustainable life’,” said Dufner. “If the Clean Planet Fund really wants to invest in companies that are sustainable, RWE should be kicked out.”

Investing in the destruction of homes and forest to mine coal

To have a better idea of the impact of RWE’s activities on the ground, we set off on a road trip 50km north of Cologne to explore the Rhenish coal kingdom: it’s the “black hole” in our “Clean Planet”, viewed from both a satellite and an investor perspective. We are in the car with Ulla Kellerwessel, who is a member of the Cologne-based association Parents for Future, and is personally involved in the RWE Tribunal initiative.

“Many people in this area lost their homes and their farmlands on our exceptionally fertile soil… [their] ability to provide food security to the next generations is seriously at risk due to the environmental disruption caused by coal activities,” says Kellerwessel. “What is legally permitted is not necessarily sustainable. That’s why the coal industry and RWE should be boycotted by green investors. I would tell all those who place their money in green funds sponsoring RWE: ‘coal kills us as you earn your greenwashed profits’.”

On the way, we paid a visit to Norbert Winzen in Keyenberg. During our conversation the fact that RWE is sponsored by Allianz, with whom Winzen has an established customer relationship, popped up. Suddenly, Winzen found himself personally, albeit unintentionally, involved in the likely greenwashing scam orchestrated by his insurance company.

It is as if the bucolic atmosphere of his centuries-old farm, surrounded by cattle grazing on pastures, suddenly collapses into the reality of the 40km2 crater of the Garzweiler mine, from which 20 to 25 million tonnes of lignite is extracted every year. Dark mountains of waste rock rise above roaring excavators digging for coal, against a backdrop of the fumes spewing from the chimneys of the nearby power stations that burn the open-cast mine’s lignite, where we and Kellerwessel had started our tour. Winzen’s farm is right on the edge of this Dantesque void, which until 2018 has swallowed up 130 villages and uprooted 44,000 people.

“We are constantly exposed to pollution, [a] digging noise and earth tremors that cause cracks in the walls,” said Winzen. He explained that his father left his first farm for the one he is now living in because of the expanding mining activities. “When I was 14, the edge of the mine was still 25km away, but then it got closer and closer, and before my eyes villages were either razed to the ground or turned into ghostly outposts like mine, as carbon-intensive power production and pollution continued,” he said. He explained why he and his family were among the 50 or 60 people still living in Keyenberg: “My village has lost most of its 900 inhabitants in the last 25 years. Since rumours spread about RWE’s plans to mine coal under our feet, at some point we also thought we’d better leave.”

Almost all the residents chose to flee after receiving compensation to buy a new home elsewhere, rather than fight in court at the very last minute with bulldozers at their doorstep and risking losing everything. The German law allows RWE to evict anyone standing on its coal concessions, provided it is to protect national energy security and after prior negotiations with landowners.

The local collective Human Rights Before Mining Rights, which represents the threatened villages, filed a constitutional court case in 2019 to overturn the provision reaffirmed in Germany’s Coal Exit Act. The plaintiffs argued that coal from the Garzweiler mine is no longer an economic necessity, as recent analysis has shown, and therefore RWE’s right to mining cannot override the right of people to live on their land.

The lawsuit was rejected, but luckily the wave of mining destruction stopped for good in October 2022, as part of a political agreement between RWE and the German government (which was albeit not legally binding). This brought forward the coal phase-out to 2030 (compared to the 2038 legal deadline), while allowing RWE to restart and delay the closure of a number of coal-fired units. The deal saved five at-risk villages and Winzen’s home, with the exception of the hamlet of Lützerath. Unfortunately, the latter was razed in 2023 despite renewed resistance, following the green light by North Rhine-Westphalia State government.

It’s not over yet, according to Dirk Tesmer from the German law firm PNT Partner, who was the lead attorney in the legal and constitutional proceedings: “In my opinion, the controversy is still ongoing because displacements occurred against the principles protecting human rights and often, without adequate indemnification,” he told Voxeurop. “People left their homes and hometowns through a painful forced process and now that five villages (where only half of the population remained) will not be demolished as initially planned, some are wondering whether they should return.” He points out that RWE has the upper hand: “Those who wish to come back worry about how to do so as a matter of law and money, since RWE owns their homes and may not be willing to give them back, while those who decide not to return will have to live forever with the knowledge that they could have stayed.”

In 2022, a study by the University of Aachen (near Cologne) revealed the deterioration of living conditions due to RWE’s eviction policy. According to Tessmer, “despite [the fact that] RWE cannot be blamed for complying with a German law which is flawed in itself, the whole process constitutes an unresolved violation of the UN Principles on human rights”. These international standards guarantee a balanced protection of landowners and business activities (2). The lawyer clarified that since they were forced to sell to RWE, the “people who left their homes in villages that are no longer affected by coal mining have the right to gain them back.”

Violation of the UN Principles should lead to an issuer’s exclusion, according to Allianz’s Clean Planet ESG safeguards (which are technically defined as “sustainability or SFDR disclosures” and prescribed by the EU legislation). These precautions are binding elements of the contract signed with investors. And yet, RWE is still in the fund’s portfolio.

***

On the way back to Cologne, the last stop on our “coal tour” with Ulla Kellerwessel is Hambach, the largest of the three coal mines operated by RWE. Crowds of visitors take selfies in front of the grandiose but apocalyptic landscape beneath, while chilling out under beach umbrellas with beds that the company installed. They are surrounded by shiny posters promoting RWE’s efforts to deploy the solar panels and wind turbines which dot the perimeter of the open cast pit.

No sign post explains that, since acquiring the land in the 1970s, RWE has cleared the Hambach forest, one of the oldest in Europe, to gradually expand the mine.

Following massive barricades by activists and court orders to protect the endangered species covered by the EU’s Habitats Directive, the company had to suspend its clear-cutting activities in 2018, but could soon resume them. RWE intends to excavate near the village of Old Manheim to obtain material for stabilising and recultivating the mine after its closure.

Dirk Jansen, managing director of the Dusseldorf-based NGO BUND (the German Association for Environment and Nature Conservation), explains that vulnerable species could still be affected: “In the area of the planned excavation there is also a small piece of forest where RWE itself has identified a summer quarter for the extremely rare Bechstein’s bat,” he said. “However, the area is still outside the scope of the current mining permit, which is due to be extended in January 2025 as part of the lignite plan adopted by the Cologne district government, allowing RWE to clear this important ecosystem.”

Surprisingly enough, Allianz invests in RWE through its Clean Planet, despite being a founding signatory of Nature Action 10, a global investor engagement initiative launched in 2023, which aims to reverse nature loss in line with the UN Global Biodiversity Framework.

Chapter III

The world of green funds plays cool in the land of coal

To justify the investments in RWE through its Clean Planet fund, Allianz bets on the company’s controversial decarbonisation plans. The climate-transition trajectory of the German utility, it should be noted, is not in line with the Paris Agreement, according to independent assessments (3). Despite investing billions in renewable energies and announcing a 27% reduction in its direct GHG emissions by 2023, RWE will continue to use lignite in the coming years. In 2023, electricity generated from coal was still equal to that generated from renewables, with a third each (the rest coming from natural gas and nuclear).

Climate transition is not enough to bring clean air

The RWE slow climate transition could lead to more premature deaths and health bills. “While fossil fuel combustion is certainly a climate crime, phasing it out to reduce carbon emissions is still not enough to save lives, given RWE’s reluctance to invest in further minimising toxic pollution from ongoing lignite burning,” Christian Schaible, head of the Zero Pollution Industry unit at the Brussels-based NGO European Environmental Bureau, told Voxeurop. In 2017, the EU adopted new standards (as part of the Industrial Emissions Directive) requiring large combustion plants to use the best available technologies to reduce their emissions. But once again, loopholes in EU legislation on industrial emissions offer a carte blanche to big polluters like RWE to get away with no substantial obligations.

Companies are free to choose from a range of more or less efficient technologies as long as they do not exceed national emission limits. “Like many other EU Member States, Germany went to the highest legally allowed pollution levels – i.e. those achievable through the less performing technologies mentioned in the EU standards – not to what is needed to protect its citizens and the environment,” said Schaible.

RWE’s latest sustainability management report states: “We are continuing to keep within the statutory limits for emissions”, and that through “the latest technology, we successfully ensured the thresholds in 2023”. The insistent reference to legal limits suggests that no more is being done than is required by law. “We can assume that RWE is going for the maximum pollution levels allowed by national law, which are way higher than the highest levels initially proposed by the European Commission’s expert group during the negotiations on the new EU standards, and [which were] eventually opposed by Germany and other countries with a strong lignite and coal industry,” Christian Schaible added. “The lax levels set in the German law have been specifically designed to allow for business as usual for lignite combustion-addicted operators such as RWE.” We reached out several times and through different channels to RWE for a comment on Shaible’s allegation. As we went to press, the company had not replied to our questions.

RWE’s alleged inaction to reduce air pollution, albeit permitted by the German authorities, does not appear to be in line with either the marketing communications or the commitments of the Clean Planet, Allianz’s “green” fund which holds shares in the German coal giant.

In terms of marketing, the teaser on the fund’s website reads: “Air pollution is responsible for around 6.5 million premature deaths every year – 9 out of 10 people worldwide breathe highly polluted air […] This is where Allianz Clean Planet comes in […] It aims to […] do lasting good for society and the environment”.

In terms of commitments, the fund’s SFDR disclosures exclude companies violating international principles, namely those set by the UN and the OECD which call for an effective mitigation of environmental damages. “Our guidelines recommend that companies should use the best available technologies, even if there is no legal requirement from a national government, in order to avoid negative impacts on people, planet and society,” clarified Allan Jorgensen, head of the OECD Centre for Responsible Business (4).

Data and experts pinpoint RWE’s untackled air pollution

The Clean Planet’s SFDR disclosures also state that the ESG portion of the investments includes only companies that do not undermine any of the environmental objectives set out in the EU Sustainable Investment Framework (per its taxonomy and related acts). RWE claims that 90% of its capital expenditure meets these objectives, but only 17% of its revenue is taxonomy-aligned, meaning that most of its profits still originate from activities classified as unsustainable, according to the EU.

The EU legislation prescribes asset managers to comply with the “do no significant harm” principle only with regard to the portion of investments declared as fully sustainable (representing a smaller share of the Clean Planet fund). Allianz has the merit to go beyond this legal requirement and, in principle, commits to exclude from its green portfolio all activities hindering “pollution control prevention”, “protection of water resources” and of “restoration of biodiversity and ecosystems” (all of which are named in the EU environmental objectives list).

Despite scoring poorly in all these three areas, as we found through data analysis and expert opinion, RWE is not banned from Allianz’s fund nor from the funds of many other asset managers which flaunt the same restrictions. The dispute about the Hambach ecosystem is only the most tangible sign of the local impact of the coal’s extraction. The invisible scourge of pollution is even worse.

According to the EU pollutant register, RWE’s coal-fired power plants account for almost 75% of the nitrogen oxides (NOx), more than 40% of the mercury and almost 25% of both sulphur oxides (SOx) and fine particulate matter (PM) emitted by all industrial plants in North Rhine-Westphalia. Fine particulate matter, in particular, comes not only from power plants but also from open-cast mines (the Garzweiler monitoring station has frequently reported levels exceeding legal limits).

In 2022 (the last year for which companies have to report to the EU), emissions of all four main pollutants are slightly higher than in 2020 (after having fallen significantly in previous years). This upward trend is confirmed by RWE’s sustainability performance report 2022 which, however, shows far lower absolute figures and does not mention mercury emissions. The company refused to explain the discrepancy (5).

Scientific studies indicate, in particular, that NOx and mercury could be reduced by up to 85% and by 36-49% respectively by retrofitting coal-fired power plants with abatement technologies (which are already used in the United States), capable of limiting emissions to the lowest levels set by EU standards. Health costs of between €93.2 and up to €213 million for mercury and €2.379 billion for NOx associated with all lignite plants in Germany could be avoided annually, while operator costs would increase by only 2%.

There was a solution, said Christian Schaible of the European Environmental Bureau: “RWE could have cut its toxic air pollutants by more than half, mostly nitrogen oxides and mercury, had it made the effort to invest in more effective pollution controls, namely the Selective Catalytic Reduction system (absent in the list of technologies mentioned by RWE), that allow meeting the EU’s most stringent limits though technically achievable and economically viable conditions.” RWE’s set targets are far less ambitious and do not cover mercury. “aiming to further reduce NOx emissions by 35 % (per MWh) [,,,] until 2030.”

There was a solution, said Schaible of the European Environmental Bureau: “RWE could have cut by more than half its toxic air pollutants, mostly nitrogen oxides and mercury, had it made the effort to invest in more effective pollution controls, namely the Selective Catalytic Reduction system (absent from the list of technologies mentioned by RWE), that allow meeting the EU most stringent limits though technically achievable and economically viable conditions.” RWE’s set targets are far less ambitious and do not cover mercury, though “aiming to further reduce NOx emissions by 35 % (per MW/h) […] until 2030.”

Most lignite plants have wasted the four years which elapsed between the adoption of EU emission standards and the enforcement deadline in 2021 without investing in cleaner technologies, thereby releasing tonnes of harmful pollutants that could have been avoided into the atmosphere.

Lauri Myllyvirta, lead analyst at the Helsinki-based Centre for Research on Energy and Clean Air, said RWE “had a moral obligation to apply the technology to reduce its emissions”. However, he points out that while the German company had plenty of time to install this technology, it is now too late to do so, because “the 2030 coal phase-out would leave little time for the new emission controls to make a difference, even if the engineering to install them was started now”.

His independent organisation estimated that the number of premature deaths expected from coal-fired power plants in Germany by 2030 (the early phase-out date for coal) could be reduced from 13,000 to 3,000 by using the most advanced technologies. The figures are however approximate and could be overestimated, as the study is based on 2017 emissions data.

RWE pollution also threatens water and soil

The environmental degradation caused by RWE also extends to water and soil, two crucial natural resources that Allianz’s Clean Planet Fund is committed to preserving. According to the BUND NGO, open-cast mining brings earth-bound sulphates (e.g. pyrite) to the surface, which react with oxygen, releasing a stream of acid that is washed into the subsoil by rain falls. Acid pollution may increase as groundwater, currently pumped out to enable coal extraction, rises again when the mines close.

BUND’s Dirk Jansen expanded on the 3,200 square kilometres of land affected as we walked along the northern viewpoint of the Garzweiler mine. “10% of land in North Rhine-Westphalia is massively affected because, every year, RWE extracts 500 million cubic metres of groundwater which will take hundreds or thousands of years to naturally return to its original level when the mining stops,” he said. “That’s why the only solution to save the surrounding wetlands is to turn the open-cast mines into lakes over the next 50 to 70 years with water piped in from the Rhine which is also contaminated.” According to Jansen: “This extra pollution adds to the ongoing acidification which the company can only control to a limited extent by covering the sulphur-rich material with large quantities of lime.” The use of water for drinking and agriculture, which has been impaired for years by coal mining, will only be possible in the future at the cost of extensive cleaning measures, he explains. The question is: “Who will pay – the company or the people?”

Similar problems arise with coal power plant ash which is disposed of in internal landfills and leads to increased concentrations of heavy metals (such as nickel and zinc). This is not to mention the mercury emitted by coal-fired power plants (the largest source of this heavy metal in Europe), which falls down to earth with raindrops, infiltrates water and land and can enter the human food chain, particularly through agriculture and fish. The EU is bound by the UN Minamata Convention to reduce mercury releases from coal-fired plants to values well below those adopted by Germany and other EU member states. In 2015, a report by the German Federal Ministry of the Environment revealed that mercury levels in waterways such as the river Rhine, which runs along the western bank of Cologne, are more than twice the level allowed by the EU (under the Water Framework Directive) and will continue to exceed the legal limit in the near future, affecting ecosystems and human health.

“We can safely say that the mercury in the Rhineland region is mostly from the airborne emissions which again are mostly from coal power plants,” said JaI Krishna Ranganathan, Senior Policy Officer for Industrial Production at the European Environmental Bureau. “In fact, the reported emissions of mercury from thermal power plants to air in North Rhine-Westphalia is at least eight times more than the total reported direct emissions into water bodies in all of Germany.”

“Without reducing mercury emissions from coal-fired power plants, the problem of excessive concentrations in the Rhine basin will not be solved,” said Cornelia Nicklas, head of the legal department at the NGO Environmental Action Germany, which together with the Brussels-based ClientEarth filed a lawsuit against the government of North Rhine-Westphalia in 2022 to enforce the protection of the local waters. “The state government did not deny that the mercury concentration in the water is linked to airborne mercury emissions from the air, but unfortunately it misjudges its responsibility for the reduction of the emissions, inter alia, with the argument that coal-fired plants meet the legal thresholds.”

ESG magic: greening everything with self-made criteria

We reached out to Allianz and shared the information we found on RWE’s negative impacts, and asked if this kind of data was considered as part of theEnvironmental, Social and Governance objectives (ESG) screening and investment decisions of the Clean Planet. We asked the insurance company about its plans to engage with RWE on these issues to monitor the company’s compliance with the fund’s commitments. Allianz did not reply to our questions, despite multiple reminders.

The European Securities and Markets Authority (ESMA) standards set a number of sustainability parameters (technically called ‘Principal Adverse Impact Indicators’ – PAIs) to measure both the negative effects of the activities conducted by the investee companies and their positive contributions to the fund objectives.

However, asset managers are bound to such indicators only as part of the overall ESG strategy, but not for the individual products they market (except for the portion declared “sustainable”). That’s why the Clean Planet fund fails to quantify the overall environmental and social impacts of its investments (which are only put into figures at a group level, aggregating all of Allianz’s products).

Asset managers are free to choose any or none of ESMA’s impact indicators or even replace them with their in-house indicators. Also, they have a wide leeway to choose their own data and proprietary rating system to determine what level of impact should trigger an engagement with individual issuers and possibly their exclusion from the portfolio.

An ESMA spokesperson explained: “The SFDR is a disclosure regulation, not a product regulation, therefore the key is that financial market participants must be transparent about how they measure the attainment of the product characteristics/ objective, through disclosing the indicators, methodologies and the data sources”.

Allianz’s environmental and social indicators at both the group’s ESG policy level and at a fund level (Clean Planet) include, among others, the reduction of carbon footprint, water emissions and hazardous waste, as well as compliance with the UN and OECD principles mentioned above (6). However, they do not consider the abatement of atmospheric contaminants which represent a major adverse impact of RWE’s activities. An Allianz spokesperson explained that this indicator is not mandatory, since “emissions of air pollutants is one of many optional PAIs (i.e. ESMA indicators) listed in […] (the) EU Regulation.”

The experts disagree, though. “It is misleading not to include the emissions of air pollutants in the Principle Adverse Impacts while claiming to address air pollution on the fund’s website,” Nicola Koch told Voxeurop. He is the head of the 2° Investing Initiative (2DII), an independent, non-profit think tank working to align financial markets and regulation with the goals of the Paris Agreement

The Clean Planet’s SFDR disclosures do not even clarify which specific data was collected directly from the issuers and from additional sources to measure the respective impacts of individual investee companies. Moreover, they state that assessments “may be subjective, incomplete, inaccurate, or unavailable”, and that “as a result, there is a risk to incorrectly […] assess a security or issuer”, with a subsequent “exposure to issuers who do not meet the relevant criteria of the Sustainable Investment Strategy” (7).

In other words there is no guarantee that the fund assessments on the adverse impact of RWE (or any other issuer) are accurate and reflect the reality on the ground.

Axel Pierron, associate director of the Morningstar/Sustainalytics rating agency, explained: “Lack of transparency on the specific data and evaluation criteria used to assess individual companies is a major driver of what is called ‘methodological’ greenwashing, as certain asset managers can be tempted to select the methodology that reduces their perimeter of investment the least.”

Sanctions targeting potential mis-evaluations are not contemplated in the EU regulation, which offers total discretion to asset managers.

A steep path ahead to clean the planet

Nevertheless Mariyan Nikolov, research and policy officer at the Brussels-based NGO Better Finance, is positive: “Once the EU financial sector-specific standards are developed, as part of the Corporate Sustainability Reporting Directive which will be enforced as of 2025, we hope to see better integrated metrics which will allow retail investors to identify relevant information in a much easier way to help them with their investment decisions”.

Improvements are also expected from the reform of the EU investor protection laws, under review, which should ensure that financial institutions and investment advisers provide accurate information to their clients.

“As part of the SFDR review we ask for the introduction of product categories with clear sustainability objectives, associated with minimum criteria, including mandatory exclusions,” explained Pierre Garrault, Senior Policy Adviser at the European Sustainable Investment Forum.

In particular, the EU legislation does not explicitly exclude green fund companies from breaching the UN and OECD standards on business conduct. An ESMA spokesperson explained that: “Financial market participants must state whether or not sustainable investments in the portfolio are aligned with these principles.” This can be done based on the fund’s internal assessment methods.

Therefore, according to the inscrutable methodology of Allianz’s Clean Planet and that of funds marketed by other asset managers, RWE may qualify as a responsible investment simply because an increasing part of its profit is generated from renewables. The negative impact that the non-renewable (coal-fired) part of its power generation has on the environment and people is arguably not factored into the sustainability equation. Still, the Clean Planet partial deviation from international standards, as well as from the 1.5 °C global temperature scenario of the Paris Agreement, is highlighted by external assessors.

“Allianz should push RWE to strengthen its transition policy, rather than justifying the investment with the expansion of the company’s renewables. Nowadays, this is a common practice in the energy sector”, said Etica Sgr’s Fabio Moliterni.

Axel Pierron of the Morningstar/Sustainalytics rating agency offers another option too: ”Allianz could for example demonstrate that it is engaging with RWE to foster the adoption of more efficient technologies to reduce its toxic pollutants with a clear roadmap and targets to achieve, and that eventually, if its attempt in encouraging change is unsuccessful, divestment will be considered.”

“Our survey shows that 50% of retail investors prefer green funds that have an impact,” said Nicola Koch of the 2° Investing Initiative (2DII). This means: “Changing the behaviour of polluting companies, which is only possible through active engagement by asset managers”.

The Clean Planet SFDR disclosures state that engagements can be “triggered by sustainability controversies”, but “there is no guarantee that the engagements undertaken will include issuers held by each fund”, as they are “closely linked to the level of exposure”. As said earlier, Allianz’s fund holds a relatively small share in RWE.

“Through constructive and critical dialogue, as well as exercising voting rights, we underline our position to transition the sector to a low-carbon energy supply,” said an Allianz spokesperson.

2DII’s Nicola Koch points out the lack of proof of how Allianz is green. “The Clean Planet Fund’s environmental impact claims can be classified as ‘unclear [and] misleading’, since Allianz explicitly advertises on the fund’s website a positive impact” he said, “but it does not provide sufficient evidence to substantiate this claim. In fact, in our impact claim analysis in 2013, several Allianz funds were also flagged due to unclear evidence.” According to 2DII’s guide, “Environmental impact claims for financial products may constitute a misleading commercial practice under consumer protection law (i.e. which are adopted by the EU – ed) […] if it contains information that could mislead the average consumer, even if the information is factually correct, […]”.

The Allianz asset manager mentions its engagement with RWE but does not clarify the if there has been any positive outcome. Also, there seems to be no record that Allianz proposed or voted on any initiative related to environmental and social issues during RWE’s general meetings.

“Disclosures under SFDR have to be fair, clear and not misleading,” confirmed an ESMA spokesperson. “National competent authorities have the investigatory powers to monitor the compliance of financial market participants with the requirements of the regulation.”

However, the Belgian financial market supervisor (FSMA) pleads helplessness, as its spokesperson told us: “The fund you are referring to (Clean Planet) is a Luxembourg fund, supervised by the Luxembourg regulator. The home supervisor of the fund is the competent authority.” Yet, during a meeting where we posed as potential clients and asked about Allianz’s investment product Better World (including the Clean Planet fund), a Crelan bank agent confidently assured us that asset managers are first checked by FSMA, since “otherwise everyone could say ‘I offer sustainable products’.”

The Luxembourg Financial Sector Supervisory Commission (CSSF) also denied responsibility, pointing out the the management company is Allianz, a German company which is supervised by Germany’s financial regulator BaFin (Bundesanstalt für Finanzdienstleistungsaufsicht). “It is up to the national supervisory authority of the management company to monitor compliance,” the CSSF spokesman said. “However, we remain the competent authority for the supervision of the fund and […] may […] discover discrepancies and […] share such information with the national competent authority and will duly consider […] supervisory work on this fund,” he said, referring to Clean Planet. ESMA clarified that the determination of the competent authority depends on the case, given the overlap between different pieces of legislation.

Norbert Winzen, instead, did not turn away from his green ethics. Back on his farm, he decided to break the silence on the fund’s questionable claims. In an email addressed in October 2024 to Allianz’s investment department, which he shared with us, he he asked the key question: “RWE will continue to mine lignite 400 metres from where I live until at least 2030. I see every day how the company is massively affecting the environment, so why should I, as an investor with sustainability principles, invest in your Clean Planet fund?”

After several weeks, an Allianz fund manager finally replied to Winzen in mid-November, he told us. The Clean Planet fund manager admitted that RWE’s coal business has a negative impact, but pointed out that the company was included in more than 500 sustainability funds. He said that the rating agencies considered its sustainability profile to be “positive”. He added that the fund had recently sold its shares in RWE, though without providing any evidence. We asked Allianz’s communication department to officially confirm this information, but we had no answer. According to the most updated holdings breakdown we obtained from the investment research company Morningstar, Clean Planet still held over 10,360 shares, worth $208,000 million, in RWE until the end of September 2024.

Stefano Valentino is a Bertha Challenge Fellow 2024.

This article is part of the investigation coordinated by Voxeurop with the support of the Bertha Challenge fellowship. With the contribution of Alef Ferreira Lopez, Data Analysis Assistant, PhD Scholar in Economics, Universidade Federal de Minas Gerais

Footnotes

1) The association between energy transition and clean air in the objectives of the Clean Planet arises from the combined statements hereafter:Fund overview

The fund invests a minimum of 90% of its assets in the shares of international companies which offer products or solutions that contribute to overcoming challenges related to three dimensions of a clean environment (clean air, clean land, and clean water).

Fund key information document

Companies engaging in work in service a cleaner environment offer products and/ or services with an active positive contribution to the improvement of challenges related to three key dimensions of a clean environment which include the core themes of clean land, the energy transition, and clean water.

2) According to the UN Guiding Principles on Business and Human Rights: “It is equally important for States to review whether […] laws provide the necessary coverage in light of evolving circumstances and whether, together with relevant policies, they provide an environment conducive to business respect for human rights. For example, greater clarity in some areas of law and policy, such as those governing access to land, including entitlements in relation to ownership or use of land, is often necessary to protect both rights-holders and business enterprises.”

3) Relevant studies include:

https://www.climateaction100.org/company/rwe-aktiengesellschaft/#skeletabsPanel2

https://www.worldbenchmarkingalliance.org/publication/electric-utilities/companies/rwe

https://www.clientearth.org/projects/the-greenwashing-files/rwe

4) According to the OECD Guidelines for Multinational Enterprises: “In particular, enterprises should [be]: identifying and assessing adverse environmental impacts associated with an enterprise’s operations, […] preparing an appropriate environmental impact assessment; […] or co-operating in remediation as necessary to address adverse environmental impacts the enterprise has caused […] Conduct meaningful engagement with relevant stakeholders affected by adverse environmental impacts associated with an enterprise’s operations […] Continually seek to improve environmental performance […], including by: a) adopting technologies, where feasible best available technologies, to improve environmental performance”.

According to the Ten Principles of the UN Global Compact: “Businesses should encourage the development and diffusion of environmentally friendly technologies. Environmentally sound technologies, as defined in Agenda 21 of the Rio Declaration, should protect the environment […]. They include a variety of cleaner production processes and pollution prevention technologies […] to reduce day-to-day […] emissions of environmental contaminants […]”.

5) A study published in 2024 shows that the risk of death from inhaling particulate matter from coal-fired power stations is more than two times higher than from other sources. Research also shows that nitrogen and sulphur oxides and particulate matter cause respiratory and cardiovascular disease, while mercury causes brain damage in human foetuses and young children. Nitrogen oxide also contributes to the acidification of water and soil, with negative effects on biodiversity, and increases the formation of secondary particulate matter (PM) and also ozone (NO2, another harmful compound).

6) The Clean Plant fund prospectus states: “As a first step promoting environmental and social characteristics, by excluding direct investments in certain issuers which are involved in controversial environmental or social business activities from the investment universe of the Sub-Fund by applying exclusion criteria. Within this process the Investment Manager excludes investee companies that severely violate good governance practices and principles and guidelines such as the Principles of the United Nations Global Compact, the OECD Guidelines for Multinational Enterprises, and the United Nations Guiding Principles for Business and Human Rights”.

7) The Clean Planet’s SDFR disclosures mentions that data is sourced from the rating agencies ISS, MSCI and Truecost and that “per each company the fund investment manager may use “one or more different third-party […] providers and/ or internal analyses”.

Allianz did not clarify which specific data was used to rate RWE against the fund’s exclusion commitments.

According to MSCI’s scoreboard, RWE is “involved in severe-to-moderate level controversies”, including the environment, human rights and impact on local communities (with no further details), and is misaligned with the environment and health sections of the UN Sustainable Development Goals (SDGs). Nonetheless, the Clean Planet SFDR disclosures pledge that all the ESG-compliant assets in the fund (including RWE) are in line with the SDGs.

Instead, the ISS considers instead that as of 2024 there is no indication of inadequate remedial efforts regarding […] relocated residents, nor any ongoing allegations of materialised impacts to community living standards”, and “there are no ongoing allegations regarding RWE’s approach to abatements and its potential negative impacts on the climate” (without considering the impact on health).

Also, nowhere is it mentioned that Allianz has access to RWE’s internal environmental management system which keeps track of the potential impacts which are not made public. The latest Sustainability Strategy Report of the German utility only shows the degree of coverage (rather than the quantity and quality of the incidents) as a performance indicator, unsurprisingly scoring 99% in 2023.