Introduction & Market Context

Wrkr Ltd (ASX:WRK) presented its Q3 FY26 quarterly cash report and activity update on April 29, 2026, showcasing significant operational momentum as the regulatory technology company positions itself to capitalize on Australia’s upcoming Payday Super reforms. The presentation comes as the stock trades at $0.115, up 4.35% and reflecting an 82.5% gain over the past year, though the company continues to invest heavily in scaling operations ahead of the July 1, 2026 legislative deadline.

The regtech firm, which aims to “make compliance effortless” through its unified platform approach, reported processing over $100 million in contributions across more than 50,000 platform sessions during the quarter, with over 6,000 organizations currently onboarding.

Quarterly Performance Highlights

As demonstrated in the company’s Q3 snapshot, Wrkr achieved several critical milestones during the quarter across both platform growth and strategic partnerships.

Wrkr reported Q3 cash receipts of $4.3 million, bringing year-to-date receipts to $11.49 million, representing 68% growth compared to the prior corresponding period. The quarter’s receipts included recurring transactional activity from Wrkr PAY, $0.7 million from PaidRight customer invoice payments following the acquisition, and $0.8 million from collection of overdue December 31 invoices.

The company highlighted major client wins including Rest Pay, which is “fully live and scaling with reduced friction for large employers,” and AustralianSuper, which achieved a production release in late March following an accelerated six-month implementation. According to the earnings call, AustralianSuper has already reached a 94% take-up rate on its production release.

MUFG’s boutique funds—LegalSuper, NESS Super, Prime Super, and BUSSQ Super—are progressing to the “Live Brand” phase, while the company’s direct-to-market initiative saw a dedicated tenant go live for the Small Business Clearing House (SBCH) transition with strong engagement from the bookkeeping community.

Strategic Acquisition Integration

The quarter’s most significant corporate development was the completion of the PaidRight Holdings acquisition, which closed on February 5, 2026, following shareholder approval on January 29.

The 100% acquisition valued at approximately $13.6 million (90.9 million shares, representing 4.8% dilution) brought PaidRight’s real-time pay compliance engine into Wrkr’s ecosystem. Post-acquisition, PaidRight contributed $0.7 million in cash receipts against $0.9 million in operating outflows during Q3, with management maintaining a full-year FY26 revenue target of $4 million for the acquired entity.

The integration status shows both platform combination and team alignment tracking “on track,” with a real-time compliance objective targeted for FY2027. The acquisition brought $1.17 million in cash balance and positions Wrkr to address complex wage compliance needs including the Better Off Overall Test (BOOT) and industry-specific tests through PaidRight’s Pay Precision technology.

Detailed Financial Analysis

The company’s financial position reflects the strategic investments required to scale operations ahead of the Payday Super reforms.

Q3 operating cash outflows totaled $6.4 million, including $0.9 million from PaidRight operations, $0.8 million in salary increases supporting 14 new full-time employees and two casual hires, and $0.2 million in legal and due diligence costs for the acquisition. Additional expenditures covered increased marketing, infrastructure, security, software subscriptions, and costs associated with relocating the Sydney office.

Strategic capital investment of $2.1 million focused on platform features for the AustralianSuper launch, SBCH solution development, data migration and management, API strategy to enable digital service provider opportunities, and Payday Super readiness.

The operating expenditure breakdown shows staff costs of $3.4 million representing the largest component, followed by administration and corporate costs of $2.4 million, product operations of $0.7 million, and minimal marketing ($60,000) and finance costs. Payments to related parties totaled $78,000 for directors’ fees.

With a cash balance of $12.48 million as of March 31, 2026, the company anticipates increased cash receipts from AustralianSuper, Rest, and boutique funds in Q1 FY27 as employer onboarding accelerates, though operating cash outflows are expected to increase in Q4 for operations, hypercare, and small business transition support.

Platform Architecture and Expansion Strategy

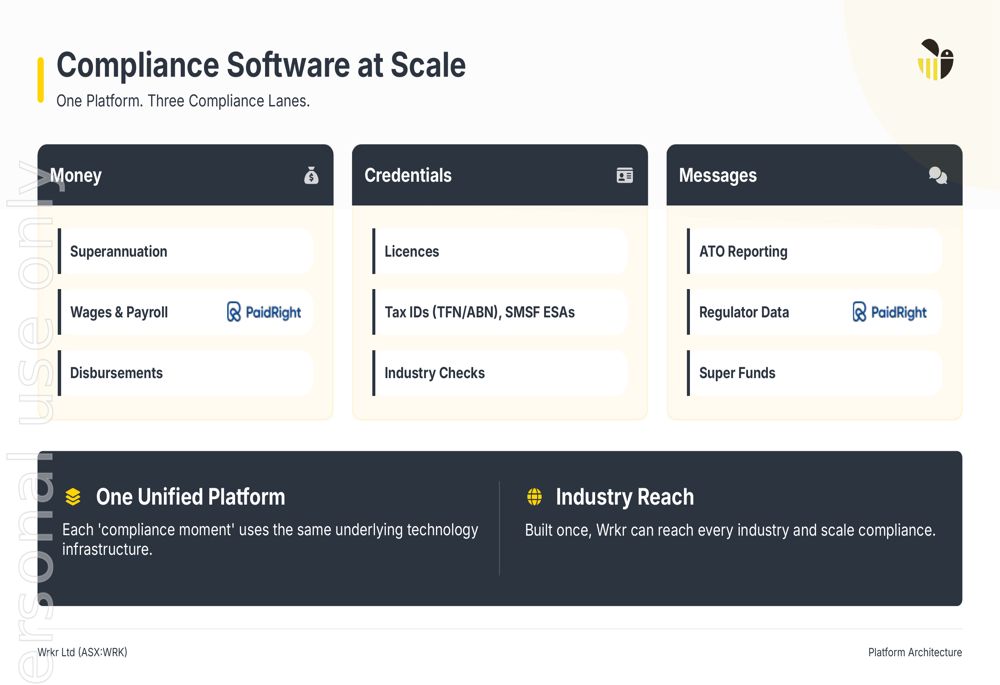

Wrkr’s competitive differentiation centers on its unified platform architecture spanning three compliance “lanes.”

The platform’s three-lane approach addresses money (superannuation, wages and payroll, disbursements), credentials (licenses, tax IDs, industry checks), and messages (ATO reporting, regulator data, super funds). This architecture enables each “compliance moment” to utilize the same underlying technology infrastructure, allowing Wrkr to reach every industry and scale compliance solutions efficiently.

The company’s market expansion strategy unfolds across four distinct phases, as illustrated in its platform reach roadmap.

Phase one focuses on super market revenues that are already proven, including fund Superstream gateway, payments, reconciliation, rollovers, ATO reporting, and employer portal features. Phase two represents strategic expansion into pay, extending super contributions to wage payments and disbursements while incorporating PaidRight’s compliance capabilities. Phase three targets scalable credential verifications including licenses, qualifications, and industry checks, with plans to scale new checks to customers in late FY2027. The fourth phase envisions direct-to-employee value-add services leveraging the pre-post tax transactional link for relevant benefits with FBT support.

Growth Initiatives and Market Positioning

Management outlined a three-pillar growth strategy focused on partnerships, direct-to-employer channels, and disciplined investment.

The partnership pillar aims to expand super fund relationships beyond Rest and AustralianSuper while positioning to white-label and scale with managed payrolls following Payday Super reforms. The direct-to-employer strategy targets the approximately 275,000 SME market and accountants servicing roughly 960,000 employees through the ATO SBCH closure, while ClickSuper migration opportunities strengthen platform stickiness and drive average revenue per user growth.

Disciplined investment focuses on increasing ARPU through targeted acquisitions in compliance moments spanning wages, licenses, and credential verification, while expanding into new markets by servicing early adopters across broader compliance needs.

Strategic integrations progressed significantly during Q3, with Workday reseller agreements finalized and SAP integration nearing completion to automate compliance for large-scale enterprise employers.

Forward-Looking Statements and Payday Super Opportunity

CEO Trent Lund emphasized the quarter’s validation of Wrkr’s execution capability: “This quarter was about proving Wrkr can deliver. Seeing large employers transition to Rest Pay and AustralianSuper is a powerful validation of our technology and our capacity to execute.”

The company’s business outlook centers on its positioning as a key beneficiary of Payday Super legislative changes, with core infrastructure already delivering for Australia’s largest funds.

Management outlined a phased implementation timeline balancing short-term dynamics with long-term strength leading to the July 1, 2026 deadline. Large enterprises are moving decisively, while mid-market adoption follows a more phased curve and small businesses remain reliant on payroll system software upgrades. The revenue trajectory indicates clear runway for growth as transaction volume transitions to the Wrkr platform, with scale-up in transaction-based revenue expected between now and December 2026, though some employer transitions may extend beyond the immediate July deadline.

Current annual recurring revenue stands at approximately $5.8 million, with management maintaining a revenue target of $50 million, though the timeline has been adjusted from earlier projections. The company acknowledges operating at a larger headcount than required long-term and faces potential delays in full fund onboarding that could impact short-term revenue targets.

Despite trading at levels InvestingPro considers potentially overvalued, the stock’s 82.5% annual gain reflects investor confidence in Wrkr’s positioning for the regulatory transition. The company faces competition from established players including Westpac QuickSuper and SuperChoice Gateway, while managing ongoing security infrastructure investments and compliance requirements as transaction volumes scale.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.

Source:

www.investing.com